It’s never pleasant to be accused of a wrongdoing you didn’t commit. Yet this happens to online shoppers when their legitimate purchases are falsely declined.

To ecommerce businesses, false declines are evidence that sometimes the cure is worse than the disease. Card-not-present (CNP) fraud can and does occur, and it’s estimated to cost online businesses more than $10 billion in 2024. But automated fraud detection tools can be overzealous, shutting down more valid transactions than fraudulent ones.

You don’t want your legitimate customers to suffer because of the actions of a nefarious few. Is it possible to stop fraud without punishing people who just want to make a purchase? It is — once you know what to look for.

In this guide, we’ll explain everything you need to know to understand what false declines are, why they happen, how much they cost you, and how to prevent them.

What Are False Declines?

Every online transaction must pass through several gateways before it’s approved, with filters at each step configured to spot the indicators of fraud.

Sometimes, one of these filters will “catch” and block an entirely legitimate transaction. This is called a false decline (or a false positive). There are two types of declines:

- Hard declines are the result of an error or issue that cannot be resolved immediately. The decline isn’t temporary, and subsequent attempts with the same payment method will likely not be successful.

- Soft declines are due to temporary issues and can be retried. Subsequent transaction attempts with the provided payment method information may process successfully.

False declines happen more often than you might expect. In one global survey, nearly 40% had a payment wrongly declined in the prior three months. That number rose to 56% for U.S. shoppers.

How Do False Declines Happen?

False declines are almost always triggered by automated fraud prevention software. If we follow a transaction through the payment chain, you’ll see that it’s checked for fraud multiple times. Each occasion is an opportunity for a false decline.

What Do Fraud Filters Look For?

Fraud filters are powered by complex algorithms that use the common characteristics of fraud as inputs. Fraud filters take things like location, delivery address, and shipping speed into account, but they go far beyond those basics. Credit card companies are reluctant to share the elements of their complex algorithms (so as not to tip their hands to fraudsters), but according to some reports, fraud-detection systems can weigh up to 500 factors.

Recent security breaches and increasing sophistication among fraudsters have made financial institutions even more assertive in their fraud prevention efforts. Banks and credit card companies have expanded their fraud criteria in the hopes of capturing more deceitful transactions — but more legitimate buyers have gotten swept up in the process.

For example, wealthy customers who shop while they travel abroad for work or pleasure may get tagged by overzealous fraud filters.

How Do Fraud Filters Work?

These are the typical steps in the evaluation of a transaction:

Step 1: The Customer Places an Order

So far, the order has been neither approved nor declined.

Step 2: The Payment Gateway Processes the Order

Depending on how they’re configured, payment gateways may run orders through a fraud filter. Typically, these filters are highly automated and unsophisticated, unable to assess “gray areas” such as unusually large purchases made for a special occasion.

Step 3: A Third-Party Fraud Protection System Processes the Order

If the business uses a fraud protection system, it involves an additional layer of automated filters to conduct a more in-depth analysis of the order. The system may use advanced machine learning techniques to “learn” the specific fraud characteristics of a business. Nevertheless, these automated systems are not infallible. For example, they may struggle with holiday scenarios, when customers place more orders than usual to be delivered to multiple addresses.

Step 4: The Issuing Bank Authorizes the Order

Banks have their own automated processes to identify fraudulent orders. When they decline a transaction, banks will provide a response code to indicate the reason, but the code can be vague.

Step 5: Settlement of the Payment

At this point, the transaction has been approved, but technical issues between the customer and the bank may still disrupt the process.

What Are the Costs of False Declines?

Imagine a false positive from the point of view of a buyer. You spend hours researching a product online, poring through reviews, comparing features, and shopping for the best deal. Finally, you decide it’s time to pull the trigger on a big-ticket item, only to have your purchase blocked. How does that make you feel about the company you had decided was worthy of your hard-earned money and exhaustive research process? Would you stick around and try your payment again (if it was allowed) or would you try your luck with the next open tab in your browser?

The main cost of false declines comes in the form of irate customers who, more often than not, take their business elsewhere — perhaps never to return — and spread news of their poor experiences through their social networks.

Here are four ways false declines can hurt your business’s bottom line:

1. Less Revenue

While many ecommerce businesses fixate on the financial impact of fraud, most don’t realize that for every $1 retailers lose to fraud, they forfeit $30 by declining legitimate consumers.

Looking at that on a national scale, one study found that online stores declined 2.7% of all incoming domestic orders because of fraud concerns in 2023. That’s $81 million lost to false declines of the $272 billion that U.S. ecommerce businesses earned in the third quarter of 2023.

2. Dissatisfied Customers

False declines aren’t simply one-off revenue hits; they tend to have a compounding effect. In ecommerce, customers are considered in terms of their lifetime value. A single loyal customer can be worth several one-and-done buyers. Losing a loyal customer doesn’t just mean losing a sale. It means losing a significant investment in marketing and customer service.

A customer’s lifetime value (CLV or CLTV) is a metric that indicates the total revenue a business can reasonably expect from a single customer account throughout the business relationship. HubSpot offers this formula:

The average customer lifespan multiplies by customer value gives you the customer lifetime value. Our research into the customer’s reaction shows that 41% of consumers will never return to your store after a false decline, and 32% say they will complain about their experience on social media.

In the luxury industry, a single customer can be worth hundreds of thousands or even millions of dollars over their lifetime. But false declines spoil the flawless, white-glove treatment affluent consumers expect.

3. A Worsened Reputation

Having a purchase declined for no apparent reason can leave a bad taste in your mouth. As Stripe.com says, false declines “can erode customer trust and dampen brand loyalty, as frustrated customers are more likely to abandon their shopping carts and turn to competitors.”

It’s a customer service truism that customers are more likely to talk about their negative experiences than their positive ones. McKinsey cites one survey that found that when consumers have a bad experience, half will complain publicly on social media. And if they don’t receive an answer at all, 81% won’t recommend that company to their friends.

These days, poor buying experiences don’t just spread by word-of-mouth. They’re enshrined for all to see on social media, product reviews and business review sites. This, in turn, shapes the decisions of future potential customers. Due to a cognitive bias called the “negativity effect,” consumers tend to perceive negative ratings and feedback as more credible than positive information.

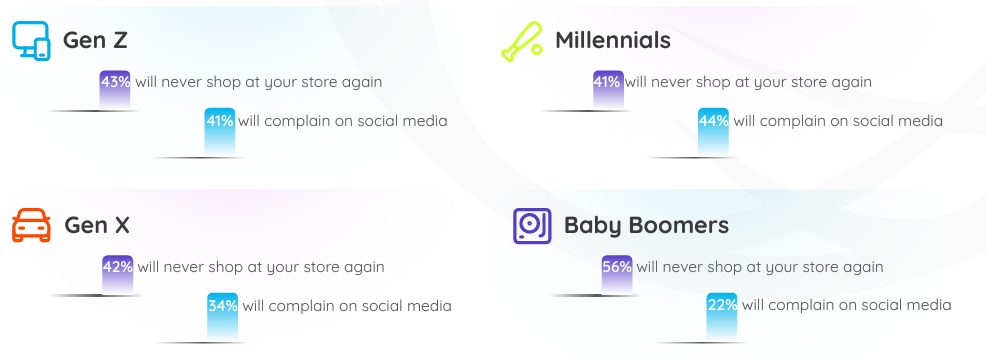

While no one is happy about false declines, there are varying customer attitudes across generations:

How To Respond to Social Media Complaints About Your Ecommerce Business

Whether it’s because of false declines, quality issues with your product, shipping delays or other problems, your ecommerce business will get complaints on social platforms. It’s a good idea to stay on top of what people are saying about your company on social media, known as “social listening,” so you can nip any dissatisfaction in the bud before it tarnishes your reputation. The Social Intelligence Lab says the “five most important social data sources for [social listening] practitioners in 2023 are Instagram, Twitter, Facebook, TikTok, and LinkedIn.”

Social listening is important now and will only become more so with time. A report by the International Council of Shopping Centers found that 85% of Gen Zers said social media influences their purchasing choices. Better for that influence to be positive, especially since Gen Z is expected to account for 52% of global online spending by 2030.

Here are a few tips:

- Be proactive. Respond early and positively to customer complaints. Don’t assume they will blow over.

- Be empathetic. Show that you really hear and understand your customers’ concerns.

- Be creative. You can turn negative comments into opportunities by demonstrating a commitment to making things better.

- Be thorough. Provide a detailed explanation of the cause of the problem and how you intend to resolve it.

- Be transparent. Resist the urge to hide or delete negative feedback; doing so may escalate the situation.

- Be human. The personal touch can go a long way toward defusing tense situations. Let your customers know they’re dealing with real people (and you see them as real people, too).

- Be accessible. Take the conversation offline, if necessary, into the realm of email or phone communication.

- Be prepared to solve the problem. Problems like false declines don’t have to be a fact of doing business online. As you’ll learn below, you can take measures to reduce or eliminate false declines so future customers will have no reason to complain.

4. Decreased Fraud Detection Accuracy

Good fraud detection depends on good data. So, ironically, declining too many legitimate transactions can lead to even more false positives. For example, if you decide to decline all purchases from a certain country – because of a few bad experiences or because you simply feel the country is too much of a risk – you won’t just lose legitimate customers. You’ll miss out on valuable transaction data that can help you make better fraud-screening decisions in the future.

If you’re experiencing an increase in false positives due to incomplete transaction analysis or the use of incomplete data sets, you may also see your fraud detection system’s accuracy become skewed over time. In the long run, this will amplify damage to your revenue and your brand.

How Can You Tell You Have a Problem With False Declines?

The truth is that you may never know for sure how many false declines potential customers experience through your ecommerce website. Unless customers tell you, you may remain blissfully unaware of how much money your fraud detection system is leaving on the table.

These options to gather intelligence on customer attitudes can be helpful in surfacing service issues like false declines:

- Monitor social media and review sites like Google and Yelp. Social listening is another valuable tool for gauging customer sentiment and catching service issues before they escalate.

- Collect voice of the customer data with surveys that collect Net Promoter Score data and other information via email, text or on your website.

- Collect and analyze the feedback customers share with your customer service and field service employees.

Another strategy is to investigate the individual details of each denied transaction to determine whether they were, in fact, fraudulent. The most reliable way to perform a fraud check is to contact cardholders directly. This process will give you insight into how many legitimate orders you’re losing to false declines, and the changes you may need to make to reduce false declines.

(If you have a high volume of transactions, it may be more practical to contact a random sample of cardholders.)

How Can You Reduce False Declines?

Giving up on fraud protection entirely would endanger your business and your customers. But it’s possible to prevent fraudulent transactions without driving away customers who get caught in the middle.

Here are some ways to lower your false decline rate while keeping your business safe from fraud.

Understand Why Declines Occur

You should know why your fraud-detection system flags and blocks purchases. What criteria does it use to identify a high-risk transaction?

Many systems will prevent certain purchases automatically, such as first-time visitors making exceptionally large orders or orders that originate in certain countries. You know your customers best. Is this kind of behavior suspicious to you? If not, optimize your system to increase the success rate of future transactions.

Reject Transactions Based on Data, Not Assumptions

Wholesale generalizations (“all orders from China are frauds,” “customers will never want to ship to multiple addresses”) are rarely based in fact. Make sure you’re making decisions based on data, not instinct. If you feel you don’t understand the data, a fraud protection partner can help.

Contact Customers Directly

A questionable transaction may be an opportunity to forge a lasting relationship with a customer. Most people appreciate the chance to explain themselves rather than being rejected outright.

Before flagging a transaction, contact your customer immediately to verify the transaction details. Your customer will appreciate that you’re looking out for them.

Rely on Technology

Advances in fraud-detection technology are made every year. The latest services use artificial intelligence and machine learning. All transactions are screened to fine-tune fraud models based on customer behavior. Transactions that pass with flying colors are automatically approved, and questionable or suspicious transactions are flagged for further review.

However, artificial intelligence still can’t match the fraud-detection capabilities of the human mind. People are unpredictable. If a customer shops in an unexpected way, making a purchase overseas, for example, it can throw a machine algorithm for a loop.

Contextual Review

Fraud analysts can help with secondary reviews of potentially fraudulent orders. They use their expertise and understanding of fraud trends to determine if a transaction is valid or not.

Secondary fraud review is just that: a team of individuals reviewing each transaction (or a selection of transactions) to detect fraud. This can be done in-house through a fraud-review team that analyzes orders, or through a third party, where the business sends orders that seem “iffy” to a vendor for them to analyze.

For example, a single fraud specialist can review multiple orders at once using group analysis. Another approach has two or three analysts working in parallel; their results are compared to make a final decision.

Technology has also expanded the resources available to reviewers. Social networks, link analysis and data visualization provide up-to-date information for reviewers to work with.

Post-Processing Audit

Machine learning/AI can also be used post-processing to validate decisions and help find patterns to be aware of moving forward. For instance, by analyzing random sets of declined transactions, analysts can measure the accuracy of automated rules and fine-tune them as needed.

The best approach to reducing false declines is combining the best of both worlds: the efficiency of automated machine learning systems with the precision and mental flexibility of expert human teams.

Acting in Real Time

Immediate gratification is the name of the game for shoppers and fraudsters today, so merchants must employ fraud prevention strategies that can quickly evaluate and react to fraud threats.

Machine learning’s algorithms can quickly and objectively identify unique fraud patterns within a merchant’s transactions. This automated analysis is a useful first line of defense to identify questionable transactions and set them aside for further review by specialized staff.

ClearSale’s Hybrid Approach

ClearSale offers a multilayered, hybrid approach to fraud prevention to combat sophisticated fraud. It starts with an AI-enabled algorithm that leverages trends, intelligence and data gathered from decades of fighting fraud in the most high-risk regions of the world. Using this technology, we can automatically approve most orders quickly.

Suspicious orders are flagged for contextual secondary reviews performed by our more than 2,000 fraud analysts who have the experience to recognize some of the hardest-to-spot fraud patterns. If necessary, our analysts may reach out to customers, but they do so in a way that demonstrates why consumers can trust your business to protect their information.

We then leverage the data gathered from those contextual reviews to help our system better distinguish valid transactions from fraud. That means our system can more easily recognize “good” transactions as we process more for the client, which increases their approval rates and revenue.

The ClearSale ecommerce fraud solution follows a four-step process that results in the lowest false decline rates in the industry.

Step 1: A Customer Places an Order

The moment a customer lands on a website page, the ClearSale system knows where the customer came from. Website orders are sent directly to us through the ClearSale application, which integrates with most major ecommerce platforms.

Step 2: Our AI Scans the Order

Our algorithm looks for common fraud patterns, leveraging a powerful, proprietary machine-learning platform, plus a series of fraud rules adapted specifically to the business. The algorithm assigns a fraud score to each order.

If the score falls within a certain threshold, the order is approved. If not, it’s sent for secondary review. (Most other systems auto-decline these orders, the majority of which are legitimate.)

Step 3: A Fraud Analyst Manually Reviews the Order

Our expert human agents are trained to see beyond the algorithm, capturing details that machines cannot. Our fraud analysts consider all the evidence, including:

- Do we have enough data to approve this order?

- Is any previous fraud associated with this customer or this product?

- What does this customer’s previous purchase behavior tell us?

- Does the customer data match up?

- Do we have any other insights from external data sources or social media?

If the analyst determines the order isn’t fraudulent, they approve the order. If not, the transaction proceeds to a second round of review.

Step 4: A Second Analyst Validates the Fraud Finding

A second analyst will take another look at the evidence, and, if necessary, will contact the customer. If the second analyst determines no fraud is present, the order is immediately approved. If they’re still unable to verify it, then, and only then, can the order be declined.

Are You Leaving Money on the Table?

Big or small, every ecommerce business is driven by two things: to grow your business and satisfy your customers. An out-of-control false decline rate can jeopardize both objectives. But with the right fraud protection partner, you can cut down on false positives or eliminate them entirely.

No matter the size of your business, fraud prevention likely isn’t your area of expertise. And it doesn’t have to be. With ClearSale in your corner, you’ll have access to the best the fraud protection world has to offer: Technology built on the latest advances in artificial intelligence and machine learning, and the kind of human expertise that only comes from years of experience.