Almost every e-commerce business would acknowledge that online payment fraud is a growing global problem—one that hurts customers and merchants alike.

But some small- and medium-sized businesses (SMBs) are uncertain about how to solve the problem in a cost-effective way and are wary of outsourcing their fraud protection. “What if,” they wonder, “we spend more on fraud protection than we were losing to fraud in the first place?”

This concern often prompts SMBs to try to keep their fraud protection in-house, screening orders themselves and spending time investigating suspicious-looking orders.

While this approach is certainly better than nothing, it’s not as economical as it may first appear:

First, it takes time away from growing your business. Every SMB owner knows the frustration of being bogged down in tedious administrative work. Every hour spent trying to figure out if an order is legitimate is an hour taken away from delighting existing customers, winning new ones, and strategizing for future growth.

Second, whether due to a lack of time or a lack of certainty, many SMB owners will err heavily on the side of caution when it comes to approving orders that seem a little off kilter. This may seem like a sensible approach, but it vastly increases the odds of false declines. Sadly, in their efforts to fight fraud, they’re creating a problem that can end up costing them much more in lost revenue—and damaged reputation.

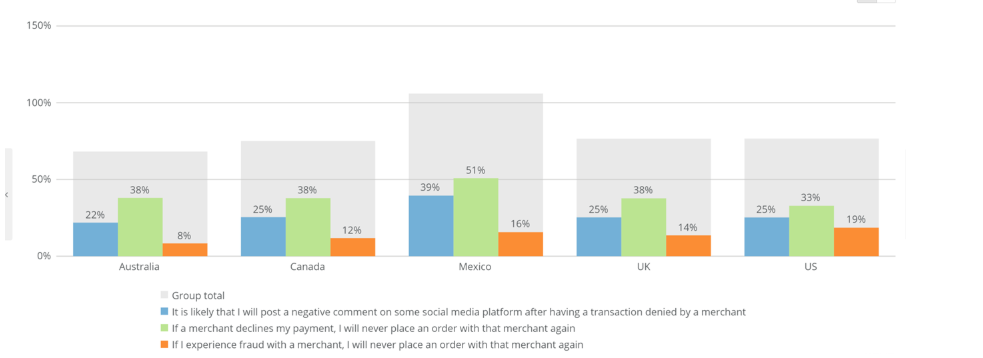

Indeed, the high cost of false declines is a key reason to consider all your options carefully when choosing and weighing the value of a fraud protection provider. The chart below, from a March 2020 ClearSale study done by Sapio Research, shows that in every market, customers would rather fall victim to fraud than have their legitimate orders declined.

SMB owners might feel caught between a rock and a hard place: Either they spend money on fraud protection (that may or may not be justified) or they spend time and energy doing it themselves, increasing their risk of false declines.

Fortunately, there’s another avenue. The right fraud protection solution—with the right pricing model—can easily pay for itself while minimizing false declines.

Pricing Options for Fraud Protection

It’s not always easy to compare the cost of fraud protection solutions because different vendors pursue different pricing strategies. There are a number of variables to consider when it comes to the price—and value—of fraud protection.

The two basic pricing options offered by fraud protection solutions are flat fees and custom pricing.

- Flat fees for fraud protection are the same regardless of the e-commerce business and its specific needs.

- Custom pricing is determined on a case-by-case basis as a result of discussions between e-commerce merchants and fraud protection solution providers. Solution providers will take into account factors such as the merchant’s industry, their long- and short-term goals, and their tolerance for risk.

Some SMBs are more comfortable with flat fees; they prefer the certainty of finding a price on the website of a fraud protection provider and knowing there will be “no surprises.” But custom pricing may be more advantageous—and profitable—because when done correctly, it can create a perfectly balanced mix of cost and benefit.

What Factors Determine the Cost of Fraud Protection?

To understand the value of custom pricing, it’s helpful to understand how fraud protection providers arrive at their prices. Any price for fraud protection has two main components: the cost of creating the solution and the value the solution provider adds to the merchant.

Already, we can start to see why one-size-fits-all pricing is a poor fit for fraud protection. The first side of the equation, the cost of creating the solution, can consist of multiple elements for performing fraud analysis, some of which certain merchants will need more than others. These can include:

- External data sources.

- The human expertise applied to machine learning, threshold definition, and the setup of rules.

- Manual review.

- Chargeback guarantees (an agreement to reimburse merchants for chargebacks, should they occur).

Consider, for example, a merchant selling consumer electronics across borders to high-risk markets such as Mexico or Russia. The electronics merchant will have completely different levels of concern regarding fraud and chargebacks than a merchant selling mattresses domestically. (Electronics, which are easy to resell, are frequent targets for fraud. Mattresses, which are almost impossible to resell, are not.)

In the example above, it may make sense for the electronics merchant to invest in more robust fraud protection measures. The mattress seller, on the other hand, may be in a position to risk a few chargebacks.

There are other sources of variability in the cost of fraud protection, as well. For example, merchants that have many recurring buyers will require less risk assessment. Merchants with frequent first-time buyers will need fraud solutions that draw on external data sources for risk analysis.

Another cost factor is the complexity of integration. Some fraud protection software integrations are essentially plug-and-play, while others require significant customization.

The Downside of Flat Fees

By now, it should be clear that the cost of a fraud prevention solution can vary on a case-by-case basis. What are the consequences for merchants who agree to flat-fee pricing? There are two:

- The merchant may end up paying more than they need to.

- The relationship between the merchant and the solution provider will not be win-win.

The following example illustrates these consequences:

A merchant is looking for a fully outsourced fraud prevention solution with a chargeback guarantee. Solution provider A charges a 1% fee regardless of the merchant’s situation and needs. Solution provider B offers custom pricing.

In this example, if the merchant goes with provider B, and the price is the same or lower than provider A, they will have clearly made the better choice. They get the same or better service for less cost.

If the merchant chooses provider B (again, the custom pricing option) and the price is higher than provider A, have they made the right choice?

In the short-term, in this example, provider A is more affordable. However, in the long-term, the arrangement may not lead to a beneficial relationship between the companies.

The merchant may come to be seen as a low- or negative-margin customer for the solution provider, and therefore, a lower priority. The merchant will get worse results from their fraud prevention solution, which translates to more chargebacks, more false declines, dissatisfied customers, and less revenue.

Additionally, there is one more risk: When offering flat-fee pricing, providers have a strong incentive to keep their own costs as low as possible, to keep their margins strong. As such, they may rely more on auto-declines for suspicious orders. After all, fraud analysts cost money, but a score decision has almost zero marginal cost. And by relying on auto-declines, the risk of false declines rises considerably.

The ClearSale Approach to Pricing

At ClearSale, we aim for long-term relationships with our clients, and we tailor our pricing to make sense for the merchants we work with. We recognize that we may not always be the least expensive option for our clients, but we do believe our customized pricing works to offer our clients the most return on their investment in fraud protection.

The ClearSale fraud protection solution never automatically declines orders. We’re proud to offer the highest order approval rates and the lowest false declines rates in the industry. For you, that means happier customers and higher profits.

Our proven experience demonstrates we can custom-fit a fraud protection solution to any business, almost anywhere. We have been a leading fraud protection provider since 2001 for local shops, as well as mega-retailers. Our 99%+ customer retention rate shows our clients are always satisfied.

Contact us today to discuss a custom fraud-protection pricing plan for your business.